Insights and Strategies

A.I. Beyond the “Magnificent Seven”…

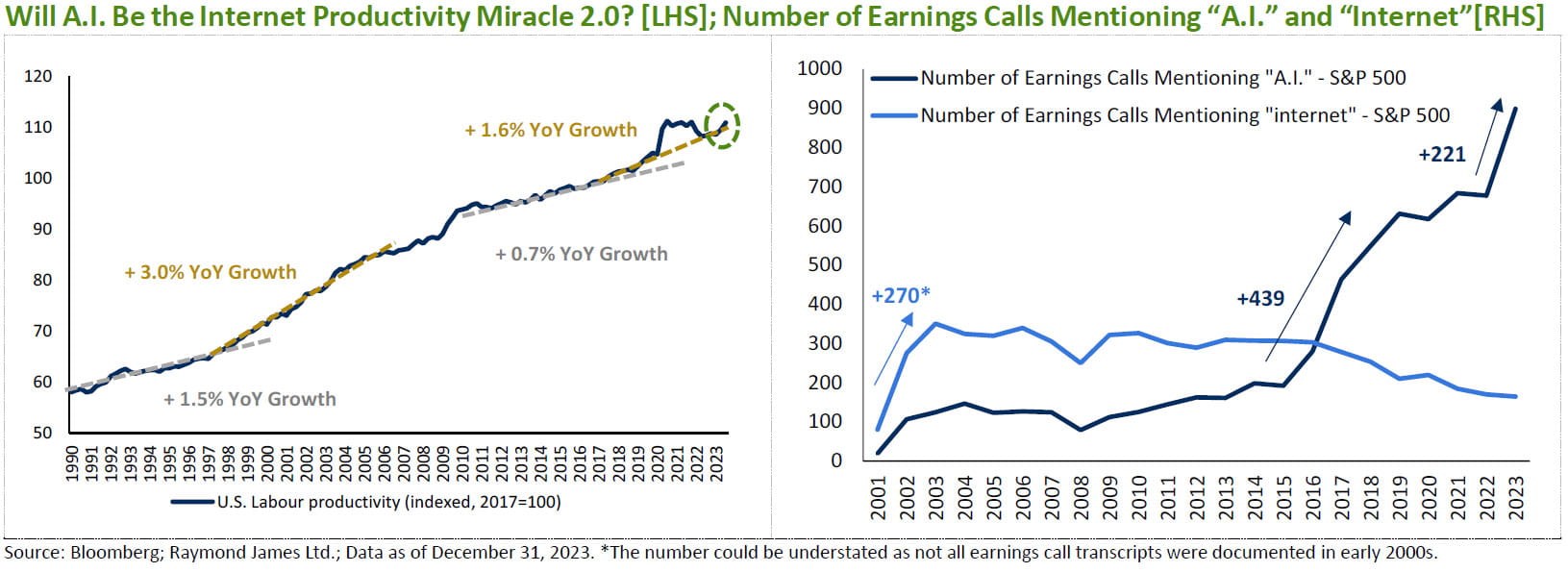

Finding a market commentary in 2023 that didn't mention the “Magnificent Seven” was quite a challenge. Artificial Intelligence (A.I.) was a significant catalyst driving the remarkable outperformance of these stocks last year. After such an impressive reaction, we must question if the exuberance is overdone in the short term, or if we see this as just the beginning of an A.I. wave, comparable to the Internet boom in the late 1990s, with an impact that could be profound and far-reaching, extending across sectors over decades. We believe the latter is more likely and anticipate numerous investment opportunities emerging across various sectors as A.I. enhances productivity and profitability, extending beyond the Magnificent Seven in the coming years. We find ourselves in an exciting era, over 70 years after Alan Turing published "Computer Machinery and Intelligence", as A.I. has more recently gained broader attention and adoption by companies outside the information technology sector, and we expect this to only accelerate.

A noteworthy parallel can be drawn when comparing A.I. to the Internet in terms of positive impact on productivity. Reflecting on the Internet's history, it was officially invented in 1983, with the adoption of Transfer Control Protocol/Internet Protocol (TCP/IP) enabling computer networks to speak to each other in a common language. However, it took over a decade to attract attention and heavy investment in new information and communication technologies. This eventually resulted in rapid productivity growth starting around 1996. As an example, as a global leader in technology innovation, U.S. productivity growth from 1996 to 2005 was substantial, with average year-over-year growth of 3.0%, even with the tech bubble bursting. Interestingly, total growth of 34% during this 10-year period matches the growth of the greater than 20-year period prior (1976 to 1995)!

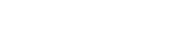

A.I. became a buzz phrase in the early 2000s, as computers challenged grandmasters in games such as chess and Go. By 2017 we saw a similar growth spurt in productivity as more public companies mentioned A.I. in their quarterly conference calls. We acknowledge that not all the acceleration in productivity can be solely attributed to technological improvement and associated capital investment, as contributions can stem from the enhancement of skills training or educational attainment as well. However, in this scenario, technology undoubtedly plays a primary role. It might be too early to definitively state there is a further boost in productivity from A.I., but the recent uptick does appear encouraging.